Embark on a journey to unravel the intricacies of Health Insurance Premium and Deductible Explained, diving deep into the world of healthcare costs and coverage. This engaging narrative aims to shed light on the essential aspects of premiums and deductibles, offering valuable insights for better understanding.

As we navigate through the realm of health insurance expenses, we will explore the fundamental concepts, their impact on healthcare access, and effective strategies to manage costs efficiently.

Overview of Health Insurance Premiums and Deductibles

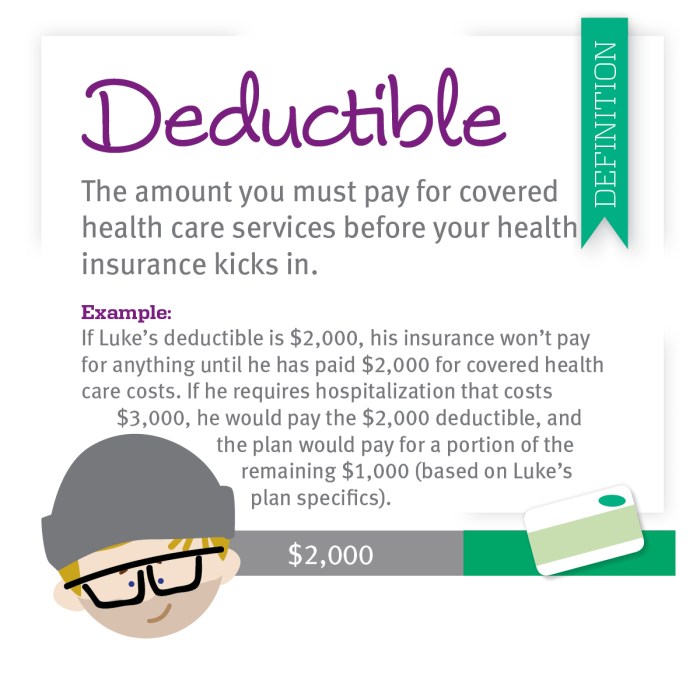

Health insurance premiums are the amount of money you pay to your insurance company on a regular basis, usually monthly, in exchange for coverage. This fee ensures that you have access to the benefits of your health insurance plan, including coverage for medical services, prescription drugs, and other healthcare costs.Deductibles, on the other hand, refer to the amount of money you must pay out of pocket for covered healthcare services before your insurance starts to cover costs.

For example, if you have a $1,000 deductible, you will need to pay the first $1,000 of covered medical expenses before your insurance kicks in to cover additional costs.Premiums and deductibles work together to determine the overall cost of your health insurance coverage. In general, plans with lower premiums tend to have higher deductibles, while plans with higher premiums often have lower deductibles.

It’s important to consider both factors when choosing a health insurance plan to ensure that you find a balance between monthly costs and out-of-pocket expenses.

Importance of Understanding Health Insurance Costs

It is crucial to have a clear understanding of the costs associated with health insurance to make informed decisions about your healthcare. By knowing how premiums and deductibles work, you can effectively manage your overall healthcare expenses and ensure you are adequately covered when needed.

Impact of Premiums and Deductibles on Overall Healthcare Expenses

Both premiums and deductibles play a significant role in determining how much you will pay for your healthcare. Premiums are the amount you pay each month to have insurance coverage, while deductibles are the amount you must pay out of pocket before your insurance starts covering costs. Understanding how these costs interact can help you budget effectively and avoid financial surprises when seeking medical care.

Tips on Managing Health Insurance Costs Effectively

- Compare different health insurance plans to find one that offers the right balance of premiums and deductibles based on your healthcare needs.

- Consider setting aside funds in a health savings account (HSA) to cover deductibles and other out-of-pocket costs.

- Utilize in-network providers to take advantage of negotiated rates that can help lower your overall healthcare expenses.

- Stay informed about your policy coverage and any changes to ensure you are maximizing your benefits and minimizing costs.

Healthcare Access and Its Relation to Insurance Premiums and Deductibles

Access to healthcare services is greatly influenced by health insurance premiums and deductibles. These costs play a crucial role in determining the level of healthcare access for individuals, impacting their ability to seek necessary medical care.

Impact of Insurance Costs on Healthcare Access

- High insurance premiums can act as a barrier to accessing healthcare, especially for individuals with limited financial resources. They may struggle to afford the monthly premium payments, leading to gaps in coverage.

- Similarly, high deductibles require individuals to pay a significant amount out-of-pocket before their insurance coverage kicks in. This financial burden can deter people from seeking medical attention, even when necessary.

- On the other hand, individuals with lower insurance premiums and deductibles may have better access to healthcare services, as they are more likely to seek timely medical treatment without facing significant financial strain.

Examples of Insurance Coverage Influencing Healthcare Access

- Imagine a scenario where an individual has a high-deductible health plan with a substantial out-of-pocket requirement. They may delay or avoid seeking medical care for a non-emergency condition due to the fear of incurring high costs.

- In contrast, someone with a comprehensive insurance plan that offers lower deductibles and copayments is more likely to proactively manage their health and seek necessary medical attention without financial constraints.

- Insurance coverage also plays a critical role in determining access to specialist care, prescription medications, and preventive services. Individuals with robust insurance plans are more likely to utilize these healthcare resources effectively.

Healthcare Providers and Health Insurance

Healthcare providers play a crucial role in the interaction between patients and health insurance companies. They are the frontline professionals responsible for delivering medical services and treatments, while also navigating the complexities of insurance coverage.

Impact of Insurance Costs on Provider-Patient Relationship

Insurance costs can significantly influence the relationship between healthcare providers and patients. High deductibles or copayments may deter patients from seeking necessary medical care, leading to strained relationships with their providers. Providers may also face challenges in delivering optimal care when insurance limitations restrict certain treatments or services.

Strategies for Choosing Healthcare Providers Based on Insurance Coverage

When selecting healthcare providers, it is essential to consider insurance coverage to ensure cost-effective care. Patients should review their insurance plans to identify in-network providers, as out-of-network services can result in higher out-of-pocket expenses. Additionally, researching provider reviews, specialties, and quality of care can help patients make informed decisions based on their insurance coverage.

Health Policies and Their Influence on Premiums and Deductibles

Health policies and regulations play a significant role in shaping health insurance premiums and deductibles for individuals. These policies can impact the overall cost of healthcare coverage and determine the financial burden on policyholders.

Government Policies and Insurance Costs

Government regulations and policies can directly impact the pricing of health insurance premiums and deductibles. For example, the Affordable Care Act (ACA) introduced regulations that required insurers to cover essential health benefits, which led to an increase in premiums for some plans.

Policy Changes and Cost Impact

- Policy changes such as the repeal or modification of certain healthcare laws can result in fluctuations in insurance costs. For instance, if a policy is changed to allow insurers to offer plans with fewer benefits, premiums may decrease but deductibles could rise.

- Government subsidies and tax credits can also influence insurance costs, making coverage more affordable for eligible individuals. Changes in subsidy eligibility criteria can impact the financial burden on policyholders.

- State-specific regulations and mandates can further shape insurance costs. For example, states that require insurers to cover specific treatments or services may experience higher premiums compared to states with fewer mandates.

Importance of Health Records in Determining Premiums and Deductibles

Maintaining accurate health records is crucial when it comes to determining health insurance premiums and deductibles. Insurance companies rely on these records to assess an individual’s health status and potential risks, which directly impact the cost of coverage.

How Health Records Influence Insurance Costs

- Health records provide a comprehensive overview of an individual’s medical history, current conditions, and any ongoing treatments. This information helps insurers evaluate the level of risk associated with covering a particular individual.

- Insurance companies analyze health records to determine the likelihood of future medical expenses. Individuals with pre-existing conditions or a history of chronic illnesses may face higher premiums and deductibles due to the increased risk of requiring expensive medical treatments.

Tips for Maintaining Updated Health Records

- Regularly review and update your health records to ensure accuracy. Make note of any changes in your health status, new diagnoses, treatments, or medications.

- Keep all medical documents organized and easily accessible. This includes test results, doctor’s notes, prescription records, and any other relevant information that may impact your insurance coverage.

- Communicate openly with your healthcare providers and ensure they have up-to-date information about your medical history. Request copies of your records to keep for your own records and share with insurance companies as needed.

Health Screening and Its Impact on Insurance Premiums

Regular health screenings play a crucial role in determining health insurance premiums. By undergoing preventive screenings, individuals can actively manage their health and potentially reduce insurance costs. Let’s delve into how these screenings can affect insurance premiums and why they are essential for maintaining overall well-being.

Relationship Between Preventive Screenings and Insurance Costs

- Preventive health screenings such as blood pressure checks, cholesterol tests, and mammograms can help detect potential health issues early on.

- Early detection through screenings can lead to timely intervention and treatment, which may prevent the development of more serious health conditions.

- Insurance providers often incentivize policyholders who undergo regular screenings by offering lower premiums or discounts on their insurance plans.

Examples of How Regular Health Screenings Can Help in Managing Insurance Premiums

- John, a 45-year-old individual, undergoes an annual wellness exam that includes various screenings recommended for his age group. As a result, his insurance provider rewards him with a reduced premium due to his proactive approach to health management.

- Mary, a 50-year-old woman, participates in a preventive health program offered by her insurance company, which includes screenings for chronic conditions. By participating in these screenings, Mary not only maintains her health but also enjoys lower insurance premiums as a benefit of the program.

- Employers may also offer wellness programs that encourage employees to undergo regular health screenings. These programs can lead to cost savings for both employees and the company through reduced insurance premiums and improved overall health outcomes.

In conclusion, delving into the realm of Health Insurance Premium and Deductible Explained unveils a complex yet crucial aspect of healthcare financing. By grasping the interplay between premiums, deductibles, and overall costs, individuals can make informed decisions to safeguard their well-being and financial stability.

Q&A

How do health insurance premiums differ from deductibles?

Health insurance premiums are regular payments made to the insurance company, while deductibles are the amount individuals pay out of pocket before the insurance coverage kicks in.

Can health insurance costs be managed effectively?

Yes, by understanding the nuances of premiums and deductibles, individuals can explore cost-saving options, such as choosing in-network providers and utilizing preventive services.

How do health policies influence insurance premiums?

Health policies and regulations can impact premiums by setting standards for coverage, pricing, and eligibility criteria, thereby shaping the overall cost of health insurance.